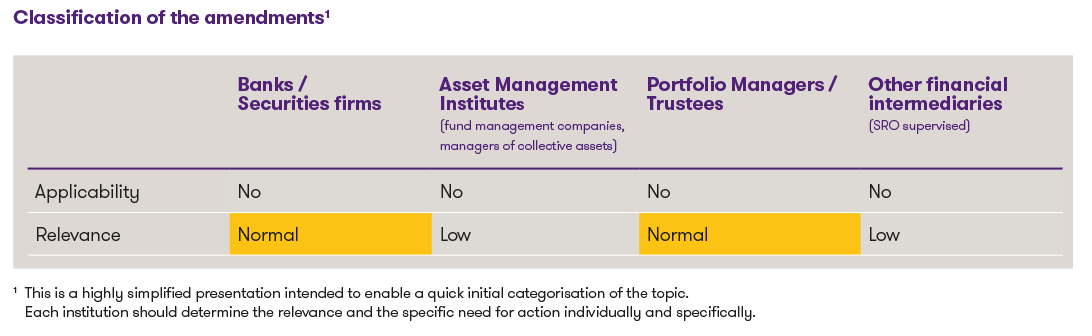

Classification of the new provisions1

![table eu gwg]()

The different types of EU legislation

The EU has various types of legislation, primarily regulations and directives. Regulations apply directly and uniformly in all Member States, while directives only set targets and leave implementation to the member states. The new anti-money laundering package comprises three regulations and one directive

Regulations of the AML package

- "AMLR": Regulation on the obligation of the private sector to combat money laundering

The regulation governs the substantive due diligence obligations of supervised entities. It replaces the five existing directives and thus introduces a uniform EU-wide regulatory framework for the first time. The provisions are generally applicable from 10 July 2027. In some cases, different implementation deadlines apply until 10 July 2029 (e.g. for professional football clubs).

The main changes introduced by the new regulation are:

Increased due diligence obligations

|

- Financial institutions must identify beneficial owners more accurately and monitor them continuously

- Enhanced due diligence requirements must be applied to very wealthy individuals

|

|

|

- Suspicious activity reports to the FIU2 must be submitted faster and more reliably

- Requests from the FIU must be answered within five days

|

|

|

- Cash payments exceeding EUR 10,000 will be prohibited throughout the EU in future

- The identity of customers must be checked and verified for payments of EUR 3,000 or more

|

|

|

New legal entities are subject to the AML legislation, e.g.

- Dealers in high-value and luxury goods (precious metals, precious stones, luxury cars, aeroplanes, yachts)

- Providers of crypto-assets

- Crowdfunding platforms

|

Standardisation of beneficial ownership

|

Uniform definition and thresholds: A beneficial owner is someone who holds at least 25% of the shares (voting rights or participation rights)

|

Register of beneficial owners

|

- Unlike in Switzerland, all EU Member States are already required to maintain their own national transparency registers

- Certain foreign legal entities will be subject to registration

- Under the new regulation, representatives of the public (e.g. the press) will also have access, provided they have a legitimate interest.

|

- AMLA: Regulation establishing a new EU authority to combat money laundering

The authority (AMLA, “Anti-Money Laundering Authority”) has already been established, is based in Frankfurt and is already operational. Six members are to sit on the board in future. Five of them have already been elected. It is planned that the authority will directly supervise 40 large and high-risk financial institutions in the EU from 1 January 2028.

- "TFR": Regulation amending the Regulation on Money Transfers

The regulation implements the FATF standards relating to the Travel Rule. The Travel Rule is an international regulation developed by the FATF (Financial Action Task Force) which, among other things, requires cryptocurrency providers to transmit and store certain information about the sender and recipient when transferring cryptocurrencies. The aim is to improve and ensure the traceability of transactions in the cryptocurrency sector. This has long been standard practice for traditional bank transfers. Unlike the other two regulations, this regulation has been applicable since 30 December 2024.

Directive on mechanisms to combat money laundering (AMLD)

After the directive came into force on 9 July 2024, it will be applicable from 10 July 2027. Member States must transpose it into their national legislation by this date. There are a few deviating transposition deadlines. This directive regulates the tasks and powers of national supervisory authorities and financial intelligence units (FIUs).

Impact on Swiss financial intermediaries

The major EU project to combat money laundering, which has been ongoing since 2021, will bring about extensive harmonisation of regulations by mid-2027 and increase the pressure on compliance. Even though Switzerland is not directly affected as a non-EU member, the new standards are relevant for Swiss financial intermediaries, especially for institutions with EU clients or subsidiaries in the EU. Stricter due diligence requirements, shorter reporting deadlines and extended transparency requirements could also become the norm in Switzerland in the medium term. It is to be expected that individual material adjustments from EU legislation could be incorporated into Swiss law in order to meet international standards and ensure competitiveness. Swiss companies and financial institutions should therefore analyse to which extent they are directly or indirectly affected by the AML package and review their systems and processes at an early stage and adapt them if necessary.

1This is a highly simplified representation intended to enable a quick initial assessment of the topic. Each institution should determine the relevance and specific need for action on an individual basis.

2Financial Intelligence Unit. This is the competent authority or reporting office for money laundering matters. In Switzerland, the MROS is the FIU.