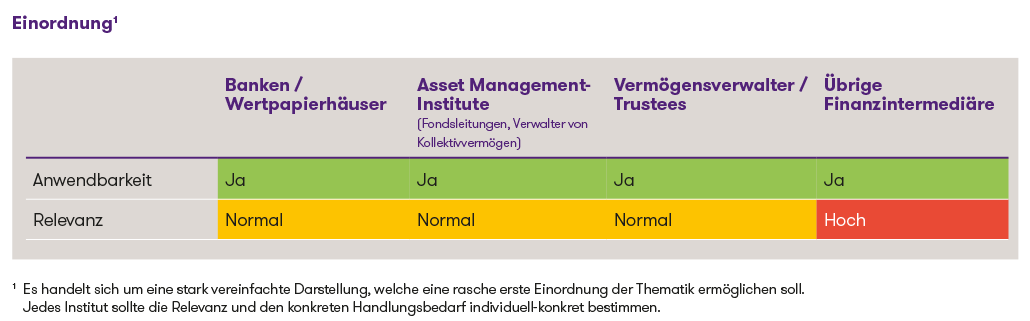

Classification1

New Requirements in the Crypto Sector

Ban on all crypto services for Russian actors

The ordinance prohibits financial intermediaries from providing any crypto‑related services to:

- Russian nationals

- Persons resident in Russia

- Russian companies

These include, among others, the following crypto services:

- Custody and administration of crypto‑assets for clients

- Operating a crypto‑asset trading platform

- Exchanging crypto‑assets for other crypto‑assets

- Executing client orders relating to crypto‑assets

- Placement of crypto‑assets

- Receiving and transmitting client orders relating to crypto‑assets

- Crypto‑asset advisory services

- Crypto‑asset portfolio management

- Transfer services for crypto‑assets on behalf of clients

Ban on Ruble Backed Crypto Assets (e.g. Stablecoin A7A5)

Ruble backed stablecoins such as A7A5 may no longer be held, traded, or transferred.

This measure aims to prevent such ruble linked tokens from being used to circumvent financial sanctions.

Ban on Transactions Involving Sanctioned Crypto Platforms

The new sanctions guidelines also include a ban on participating in transactions if they are conducted through sanctioned crypto service providers or platforms. This includes, in particular, the provision of wallet or account access, technical support services, and the use of sanctioned trading venues.

Existing Exemptions

Crypto services may still be provided to:

- Swiss nationals

- EEA and UK nationals

- Holders of CH/EEA/UK residence permits

This applies even if these individuals also hold Russian citizenship, provided they reside in Switzerland or in the EEA/UK.

Practical Implications for Financial Institutions

With the adoption of the 19th sanctions package, the crypto sector has become a mandatory sanctions risk that financial intermediaries must monitor. Institutions must expand their existing sanctions controls and adapt their operational processes accordingly.

Customer Files & KYC

- Sanctions screening must include crypto-related transactions.

- Verification of nationality, residence, beneficial owners, and ties to Russian companies.

- In-depth due diligence for complex structures or intermediaries.

Monitoring & Token Screening

- Token-level checks (ruble-backed stablecoins, sanctioned crypto assets).

- Updating screening tools.

Governance & Ownership Structures

- Verify whether Russian individuals hold control or ownership rights.

- Exclusion of Russian board members or controlling persons.

- Obligation to provide documentation to supervisory authorities.

Handling of Existing Wallets and Crypto Assets

- All crypto services provided to sanctioned individuals are prohibited

- Existing wallets and crypto accounts must be actively closed. Simply freezing them is not sufficient.

- Return of funds to customers, or

- Conversion into non-sanctioned assets (e.g., fiat currency), where legally permissible, as well as

- Compliance with deposit restrictions.

Reporting Obligation to SECO

Financial intermediaries are required to report to SECO all crypto transactions, wallets, or token connections where links to sanctions are identified or suspected.

Conclusion

With the 19th sanctions package, the crypto sector is being fully integrated into the Swiss sanctions regime for the first time. Financial service providers should expand their sanctions frameworks to include token, platform, and ownership aspects, adapt KYC/AML processes, review governance structures, and implement technical control mechanisms to consistently reduce regulatory and operational risks.

1This is a highly simplified overview intended to provide a quick introduction to the topic. Each institution should determine the relevance and specific need for action on a case-by-case basis.