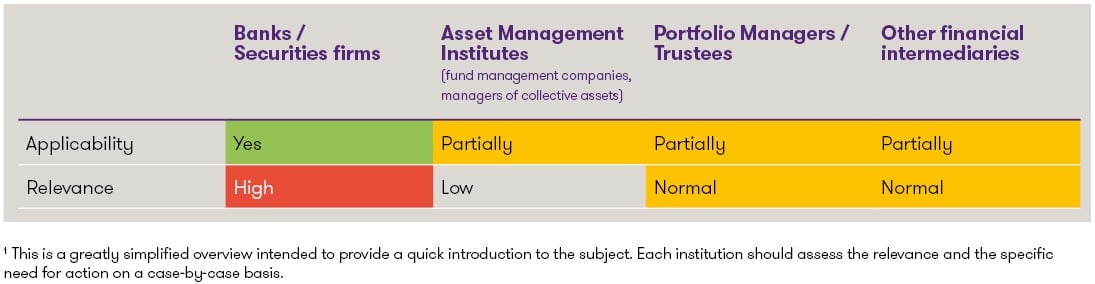

Classification1

1This is a greatly simplified overview intended to provide a quick introduction to the subject. Each institution should assess the relevance and the specific need for action on a case-by-case basis.

The partial revision introduces five practical changes in particular:

- Explicit enshrinement of the prevention of breaches of coercive measures under the Embargo Act (EmbA) as an additional purpose of the AMLO-FINMA.

- An explicit obligation to be able to trace and understand the ownership and control structure of the contracting party (previously“merely” part of FINMA’s supervisory practice).

- Specification of organisational measures to prevent violations of the EmbA (including risk analysis, internal guidelines and, where applicable, screening systems).

- Correspondent banking relationships / payable-through accounts: Payments for end customers of the correspondent bank may only be executed if the correspondent bank can provide relevant KYC/CDD information upon request.

- Sub-accounts: For sub-accounts held by individual clients, a declaration regarding the beneficial owner must always be obtained (clarification in accordance with Art. 4 AMLA and FINMA practice).

The partially revised AMLO-FINMA is planned to come into force on 1 January 2027, at the same time as the revised Code of Conduct (CDB 27).

Overview of the key changes

The EmbA/sanctions are explicitly included in the “purpose” of the AMLO-FINMA (Art. 1 para. 1 nAMLO-FINMA)

The scope of the AMLO-FINMA is expanded to include the prevention of breaches of coercive measures under the EmbA. This means that “sanctions compliance” is not only understood as a general legal/reputational risk within the governance framework, but is, for the first time, visibly and directly enshrined in the AMLO-FINMA.

Transparency of the ownership and control structure (Art. 9b nAMLO-FINMA)

Financial intermediaries must be able to trace and understand the ownership and control structure of the contracting party. The FATF had criticised the fact that no explicit general standard had existed for this purpose to date. Although FINMA had already required this in its supervisory practice, the new provision now codifies this practice at the ordinance level and thereby promoting legal certainty.

New focus on organisational measures to prevent violations of the EmbA (Art. 30 nAMLO-FINMA)

FINMA is introducing a specific provision that clarifies the organisational measures for preventing breaches of sanctions regimes (i.e. breaches of the EmbA). The explanatory report emphasises that supervised institutions are already required to adequately identify, monitor and mitigate their risks arising from sanctions regimes (including within the framework of their ICS and risk management). The new standard specifies this obligation in the context of the AMLO-FINMA. The report also notes that the AMLA revision implements the FATF recommendations on proliferation financing and that organisational measures may include, in particular, risk analyses, internal guidelines and (depending on size and activity) IT-supported screening of business relationships/transactions.

Correspondent banking relationships: Payable-through accounts (Art. 37 para. 3 and 5 nAMLO-FINMA)

Correspondent banking relationships are banking services provided by one bank (‘correspondent bank’) on behalf of another bank (‘respondent bank’). The risk in such arrangements is that the correspondent bank does not maintain a direct customer relationship with the respondent bank’s customers. FINMA has now clarified the regime for such services: in the case of payable-through accounts, the correspondent bank may only execute payments for the respondent bank’s end customers if it is ensured that the respondent bank can provide all customer information necessary for due diligence purposes upon request. According to FINMA, this is in line with long-standing supervisory practice and addresses FATF requirements.

Sub-accounts: Declaration regarding the beneficial owner is always required (Art. 65 para. 2 let. d nAMLO-FINMA)

In the case of sub-accounts for individual customers, it is expressly clarified that a declaration from the contracting party regarding the beneficial owner must always be obtained and verified. The explanatory report justifies this, among other things, on the grounds of risks that could otherwise “hardly be controlled and limited” and locates the obligation in the requirements of Art. 4 AMLA (identification/verification of the beneficial owner).

Timetable and regulatory process

FINMA launched the consultation on the partial revision of the AMLO-FINMA on 12 May 2026. It will run until 9 June 2026 and is therefore rather short. The reason for the shortened deadline is that the amendments are intended to come into force before the next FATF evaluation, which is expected to take place between May and July 2027. Once the consultation is completed, FINMA will evaluate the comments received and define to which extent the proposed amendments will be implemented.

Conclusion and practical implications

Although FINMA notes that no further implications are expected at the level of FINMA regulation (as key obligations already exist under the law or on a principles-based basis), the proposed changes to the AMLO-FINMA will, in practice, entail a significant need for review and adaptation depending on the institution and business model, particularly in the following areas:

- Sanctions/EmbA governance: Integration of sanctions risks into risk analyses, guidelines, controls and (where appropriate) screening mechanisms.

- KYC/structural transparency: Systematic understanding and documented traceability of ownership/control chains, including complex structures.

- Correspondent banking business: Operationalisation of the correspondent bank’s ‘information-on-request’ capability for payable-through accounts (data delivery capability, processes, SLAs/contractual clauses, escalation).

- Sub-accounts: Ensuring that, for sub-accounts held by individual customers, the beneficial owner declaration is consistently obtained, verified and documented.

Our support

Grant Thornton assists companies in understanding regulatory changes and supports them in their practical implementation. We are also available as a point of contact for the conceptual and technological aspects of implementation.