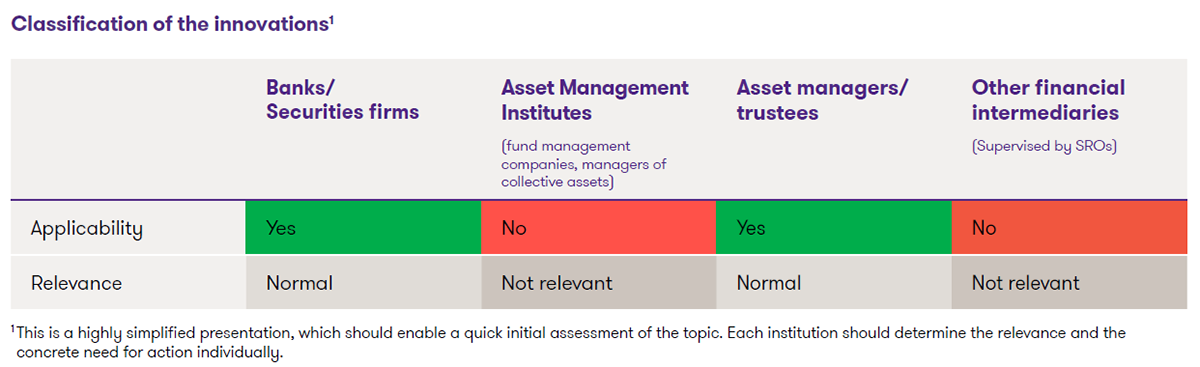

Classification of the innovations 1

1This is a highly simplified presentation, which should enable a quick initial classification of the topic. Each institution should determine the relevance and the concrete need for action individually.

What are the most important provisions of the ordinance for asset managers and what does this mean in practice? The article provides an overview based on the following structure:

- Scope of the ordinance

- Client onboarding

- Permitted investments (subdivision according to Art. 6 and 7 VBVV) and authorisation by the Child and Adult Protection Authority (KESB)

- Reporting

Scope of the Ordinance

The VBVV is primarily aimed at the mandate holders, i.e. the guardian or conservator of the person concerned (i.e. the person under guardianship or conservatorship).

For asset managers, however, the ordinance is relevant in that certain provisions must be observed both in the process of client onboarding and in the ongoing servicing of the client.

The VBVV does not apply to advance care directives but may be used as an aid to interpretation within the framework of such directives.

Client onboarding

The mandate holder acts vicariously towards third parties in the name and for the account of the person concerned. Asset managers must therefore treat the person concerned as a client and conclude the contract in his or her name. Cases in which the mandate holder or even the KESB acted as a contracting party, which were partially tolerated in the past, are now no longer permissible.

In practice, this means that all obligations associated with the contracting party must be carried out for the person concerned, such as, for example, identification, creation of the customer and risk profile, comparison with sanctions lists, etc. When choosing the investment, the personal circumstances of the person concerned must be taken into account, in particular age, health, subsistence needs, income and assets as well as insurance cover. The will of the person concerned must also be taken into account as far as possible. Any insurance benefits, in particular in the event of retirement, accident, illness or need for long-term care, as well as any other vested rights, shall be included. The investment must be chosen in such a way that the funds are available for normal living expenses and for expected extraordinary expenses at the time of need.

The following duties in particular are relevant vis-à-vis the mandate holder:

- Although not specifically prescribed, both the mandate holder and the contracting party should be identified.

- The basis for representation (authorisation by the KESB) should be checked and documented.

- As an authorised person, the mandate holder should also be formally checked against sanctions lists.

If knowledge and experience are relevant for the fulfilment of the FinSA obligations, e.g. for client segmentation, the knowledge and experience of the mandate holders can be taken into account.

In addition, the conclusion of asset management contracts, which also include investments for further needs (cf. following section), requires authorisation by the KESB. It is recommended to check and document the existence of the same.

Permitted investments and authorisation by the KESB

The permissible investment options for securing ordinary subsistence (Article 6) and the investment options for more extensive needs (Article 7) have been expanded. In particular, this promotes the possibility of diversification. Investments that are not included in the lists may be approved by the KESB under certain conditions in the event of particularly favourable financial circumstances.

If assets that exist at the time the guardianship or conservatorship is established and assets that accrue to the person concerned after that time do not meet the requirements of Articles 6 and 7, they must - with a few exceptions - be converted into permissible assets within a reasonable period of time. The conversion must take into account the economic development, the personal circumstances and, as far as possible, the will of the person concerned.

The making of investments to secure ordinary subsistence (Art. 6) does not in principle require authorisation by the KESB, since the investment activity is part of the ordinary tasks of a mandate holder. However, the general principles under Article 2 must be taken into account. Thus, within the framework of the investment of assets, it must be ensured that the assets are invested safely and, as far as possible, profitably, that the investment risks are minimised through appropriate diversification and that any fees incurred are in reasonable proportion to the assets invested and the expected return. This does not mean that the most costeffective solution should always be chosen. Rather, nonnecessary fee-triggering reallocations should be avoided where comparable solutions are also possible.

If the mandate holder is of the opinion that the personal circumstances of the person concerned permit an investment in assets for further needs under Article 7, he or she must make an asset segregation which is submitted to the KESB for approval. The asset segregation may be made in the form of an investment proposal and should clearly show the separation of assets under Articles 6 and 7. The KESB must also decide which assets and investments the mandate holder may dispose of independently or only with the KESB’s authorisation on behalf of the person concerned.

Reporting

The unsolicited reporting from financial institutions to the KESB has been abolished. The required information should be obtained from the mandate holder. In individual cases, however, the KESB has the right to obtain information directly from the bank, the asset manager or the insurance company by means of an order. This applies in case of a particular urgency and if the interests of the persons concerned can only be protected in this way (precautionary measure).

Conclusion and possible need for action

The totally revised ordinance enters into force on 1 January 2024. It will be applied in advance by the KESB and in particular by the mandate holders concerned. The Conference for the Protection of Children and Adults (KOKES), together with SwissBanking, will draw up and publish recommendations for practice in due course.

For asset managers, it is advisable to review the client forms and the financial circumstances of the persons concerned. If necessary, the client forms must be updated and the investment in assets for further needs must be requested from the KESB via the mandate holder. Furthermore, for all asset management activities that require authorisation by the KESB, it must be ensured that this is available and should be kept on file accordingly.